Which Batteries Will Fuel the EV Adoption?

Canadian Critical Minerals Ecosystem (Post 2)

Over the last 10 years we have seen the growth in EV sales balloon from 55K in 2011 to nearly 7 million in 2021. Unsurprisingly this has coincided with a boom in the demand for lithium and other critical minerals used in the production of EV batteries. This begs the question: are the inputs in today’s battery chemistry here to stay or will a new technology turn the demand equation on its head? In this post we will take a look at the staying power of the battery types behind the surge in EVs and examine some of the new technologies that could change the battery landscape as we know it.

Where Are We Now?

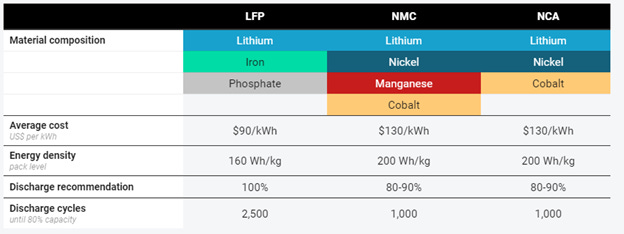

The most widely used battery in today’s EV is the NMC (nickel-manganese-cobalt) due to its high energy density as well as its ability to hold a charge in colder climates. Similar to the NMC chemistry the NCA (nickel-cobalt-aluminum) is also used in longer range EVs and have similar capacity in colder conditions. The pushback on these two battery types is cost, both upfront as well as social, which is driven by the inclusion of cobalt. Not only is Cobalt the most expensive metal used in these batteries it also has some indirect costs. Over 70% of its production comes from the Democratic Republic of the Congo where artisanal mining (child labour, high levels of pollution, high negative social impact) is estimated to contribute roughly 20% of total production. Check out this clip from the Joe Rogan Experience for more information on the situation in the DRC.

In a move to lower these costs there has been a shift by major EV producers to the LFP (lithium-iron-phosphate) battery. While these batteries are cheaper per kWh and have a significantly higher cycle life (the number of times the battery can be charged/discharged) these advantages come at the cost of overall capacity which is further reduced in colder weather. To offset this limitation in range, manganese is being introduced into some battery chemistries, but the LFMP batteries have yet to gain commercial adoption.

Source: here

Who’s Driving?

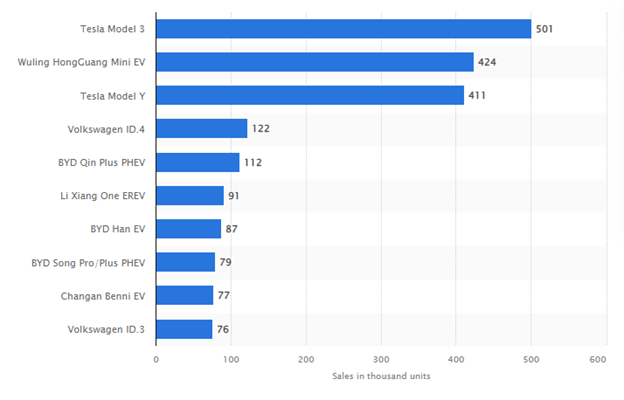

In order to figure out what the battery type of choice is today we have to take a look at the top EV manufacturers, largely comprised of Tesla, Wuling and VW. In late 2021, Tesla announced that it would be switching to LFP batteries in all of its standard range Model 3 and Model Y vehicles. The Wuling HongGuang Mini EV is the best-selling model in China and uses an LFP battery as does another Chinese manufacturer, BYD. This should come as no surprise since over 65% of all EVs in China are built with LFPs. VW has also signalled that it will be adopting the LFP battery in its entry level models. Overall demand for LFPs looks to continue its growth with some estimates have LFPs accounting for over 50% of the global market by 2030.

Top 10 Global EV Sales 2021

Source: here

Where Are We Going?

Predicting what will be the dominate battery technology of the future is an exercise in not knowing what we don’t know but there are a couple of chemistries that are getting some attention. The first is Lithium-sulfur (Li-S) which offers a specific energy of 3 times that of an NMC battery. Since sulfur is readily available the cost for an Li-S battery would be materially cheaper than current technologies. The other notable technology is the Sodium-ion (Na-ion) which would also greatly reduce the cost in production, although the low cycle count and issues with expansion in the cell when fully charged currently prevent this technology from being adopted.

Key Takeaways

Anyone waiting for a new technology that’s going to upend the Lithium demand picture is going end up feeling like they are waiting for Godot. When coupled with the demand from the renewable energy buildout the demand case for lithium looks to remain strong for the foreseeable future. The same can’t be said for cobalt and nickel which is already being phased out in lower end EVs by several manufactures however as the overall demand for EVs grows, use of these metals will persist.